How Can Credit Unions Use Digital to Improve Member Experience in their Wealth Management Program?6/24/2024

Digital engagement has become a standard expectation of almost every service and product in the current marketplace. Digital tools and workflows can be tailored to create a quick, easy, and pleasant experience for credit union members, yet this area is often neglected - especially within wealth management. To remain competitive and meet the expectations of today's members, credit unions need to focus on the digital experience of their wealth management programs. Three key areas credit unions can make strategic initiatives include: digital account opening, data analytics, and mobile user experience.

1. Streamline Digital Account Opening Traditional paper-based onboarding is time-consuming and error prone, creating a cumbersome member experience. On the other hand, a streamlined digital account opening process reduces friction and complexity for members. Credit unions that implement a truly digital account opening process can significantly enhance the member onboarding experience, making it simple and hassle-free. Key features to implement include:

2. Mobile First User Experience A superior mobile user experience is crucial for engaging members who increasingly rely on smartphones and tablets for managing their finances. Credit union wealth management should focus on creating a mobile app that offers full functionality. Important aspects include:

Scottsbluff, NE — Sugar Valley Federal Credit Union has partnered with Credit Union Wealth Group to offer fiduciary financial planning and investment management services to its members. Sugar Valley FCU treats its members like family and continues efforts to provide competitive rates, a variety of loan options, and a family-oriented banking experience for the community. The wealth management program will provide members with fiduciary investment services and access to dedicated financial advisors. The full service program provides support for the credit union, including: program management, marketing, compliance, technology and back office support. All members are invited to work with the financial advisors at their own convenience.

Members who work with the financial advisors will have access to a variety of services. ● On-demand, dedicated financial advisors ● Managed investment portfolios ● Financial planning, investment management, & estate planning services ● Digital onboarding and member portal ● Retirement & life event planning ● Retirement plans for business clients Megan Ogburn, Manager/CEO at Sugar Valley Federal Credit Union, on the partnership: “Our main function as a credit union is service to our members to aid in the furthering of their financial journey. A partnership with CU Wealth will give us one more critical tool to assist our members in every step of that financial journey. We feel that of all the options out there CU Wealth aligns best with our daily mission.”  The foundation of any successful wealth management program is a thorough understanding of the financial situation and needs of the members it is designed to serve. This means going beyond basic demographic data to grasp the nuanced financial goals, challenges, and behaviors of their members. The journey toward successful wealth management offerings begins with gathering a wide range of member data and insights.

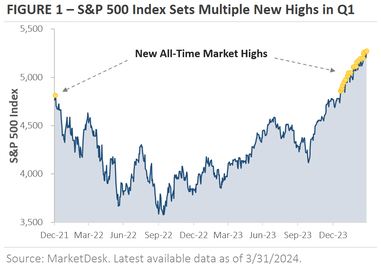

Gathering Insights: A Multifaceted Approach Credit unions can leverage many tools and strategies to gather insights, including: Teller Insights: This is the front line. Tellers regularly engage in conversations with members, providing them with a firsthand look at members' immediate financial concerns, questions, and the types of transactions they prioritize. This direct feedback is invaluable for identifying trends and areas where members may require additional support or services. Select Employer Group Findings : SEGs typically have unique retirement plans and benefits packages that play a significant role in a member’s financial life. By gaining a deep understanding of these specifics, credit unions can offer highly personalized wealth management services that align with the unique needs and opportunities of their respective SEGs. Transactional Data Analysis: Reviewing transactional and financial data can help credit unions identify patterns and trends that speak to broader financial behaviors and needs. Surveys and Questionnaires: These can uncover specific financial goals, preferences, and concerns of members. Open-ended questions can provide valuable context and insights into the why behind member behaviors.  Key Updates on the Economy & Markets Stocks continued their upward trajectory in early 2024. The S&P 500 returned more than 10% for a second consecutive quarter, setting multiple new all-time highs along the way. Notably, this quarter saw a significant shift in sentiment, as investors now only expect three interest rate cuts this year as compared to six at the start of the year. This change in expectations came as inflation progress slowed and the U.S. economy continued to expand despite higher interest rates, both of which signal a need for fewer rate cuts. This letter recaps the first quarter, discusses the stock market’s strong start to 2024, and looks ahead to the second quarter.  S&P 500 Sets 22 New All-Time Highs in Q1

The stock market is off to a strong start this year, with the S&P 500 Index gaining +10.4% in the first quarter. Figure 1 graphs the price of the S&P 500 Index since the end of 2021. The yellow dots mark new all-time closing highs. On the far-left side of the chart, the single yellow dot marks the previous all-time closing high set on January 3rd, 2022. Shortly after the January 2022 all-time high, the Federal Reserve started its campaign of aggressive interest rate hikes as inflation spiked to a 40-year high. The chart shows the 2022 stock market selloff as investors feared that higher interest rates would slow the economy. The January 2022 all-time closing high held throughout all of 2022 and 2023, but it’s already been eclipsed multiple times in 2024. After trading below its prior all-time high for over two years, the S&P 500 Index has set 22 new all-time closing highs this year. The yellow dots on the far-right side of the chart mark these new highs and show the S&P 500’s steady climb higher in early 2024.  Credit unions have long stood as beacons of member-centric service, fostering relationships built on trust, transparency, and a commitment to the financial well-being of their members. As wealth management programs become increasingly integral to the services offered by credit unions, the adoption of a fiduciary-driven sales culture is not merely a regulatory requirement but a strategic imperative that aligns with the core values of credit unions. This article delves into why establishing such a culture is crucial for maintaining the delicate balance between offering comprehensive wealth management solutions and preserving the trust and loyalty that defines the credit union member experience.

The Fiduciary Standard: A Cooperative Value At the heart of a fiduciary-driven sales culture lies the fiduciary standard, which mandates that financial advisors act in the best interests of their clients, above all other considerations. This standard is especially resonant within the framework of credit unions, where the ethos of member-first is foundational. By embedding this principle into the DNA of their wealth management programs, credit unions can underscore their commitment to offering advice and solutions that genuinely align with the individual financial goals and needs of their members. Aligning with Credit Union Values Credit unions are unique in the financial world due to their cooperative structure; they are owned by their members, and their primary mission is to serve these members rather than to generate profits for external shareholders. A fiduciary-driven sales culture reinforces this mission, ensuring that wealth management services strengthen, rather than undermine, the core values of mutual benefit and member welfare. This alignment fosters an environment where members feel valued and understood, crucial factors in building long-term relationships and member loyalty.  Monthly Market Summary

Stocks Trade Higher for a Fourth Consecutive Month, While Bonds Trade Lower

Stocks traded higher in February, with the rally broadening after large cap stocks accounted for most of January’s gains. The S&P 500 traded above 5,000 for the first time, setting a new all-time high, and has now returned +21.5% since the start of November. The Dow Jones Industrial Average set a new closing high in February, and the Russell 2000 Index of small cap stocks outperformed the S&P 500 after trailing by -5.5% last month. The Consumer Discretionary, Industrial, and Material sectors outperformed the S&P 500, while the Utility, Consumer Staple, and Real Estate sectors underperformed. In the credit market, bonds traded lower for a second consecutive month as two themes caused rates to rise. First, the Federal Reserve told investors it wants more confirmation that inflation will return to its 2% target. This statement effectively pushed back the timing of the first interest rate cut. Second, multiple inflation reports were hotter than expected, hinting at sticky inflation. This year’s bond sell-off suggests the market got ahead of itself by forecasting too many rate cuts. Investors now expect three rate cuts this year, a decrease from the forecast for six rate cuts at the start of the year.  In today’s digital world, credit unions should be continually seeking innovative ways to enhance member services and deepen member relationships. An often overlooked and missed strategy is leveraging consumer-permissioned data to tailor product and service offerings to the membership. The biggest challenge for the credit unions that try to implement this strategy is the data accessibility. Credit unions often do not have the data collection technology or the members’ desire to share data due to no perceived value. One solution for credit unions is to utilize their wealth management offering to gain access to the required consumer-permissioned data.

Members are often motivated to share data with their financial advisor and online wealth platform by a combination of factors which revolve around trust, personalization of services, and the value they derive from the advisor-client relationship. Logically, the more information a member can share with his/her advisor, the more personalized the advice they will receive. Superior financial advisors gather a wealth of data in the course of their client interactions, which, when shared ethically and securely with credit unions, can lead to more personalized and effective financial solutions. Below, we aim to explore the types of data collected by financial advisors and how this data can be shared responsibly with credit unions to benefit members. Financial advisors have access to a myriad of data on a continuous basis that provides deep insights into a member’s financial life. This can be securely collected and shared to mutually benefit the member and the credit union.  Monthly Market Summary

Stocks Trade Higher in January, Propelled By Continued Mega-Cap Strength

Stocks traded higher to start the new year, with the S&P 500, NASDAQ 100, and Dow Jones Industrial Average each setting new all-time highs. In continuation of last year’s trend, the companies with the biggest market caps accounted for a substantial portion of the early-year gains. This leadership can be seen in the January returns of various factors, including the Russell 1000 Growth’s +2.4% return and the NASDAQ 100’s +1.8% return. In contrast, smaller companies traded lower, with the Russell 2000 underperforming the S&P 500 by -5.5%. Bonds produced flat returns after a robust Q4, when Treasury yields fell in anticipation of rate cuts by the Federal Reserve. When could the first interest rate cut arrive? The section below provides an update on monetary policy after the Federal Reserve’s January meeting.  When looking to offer wealth management programs, credit unions are often faced with a choice between a third party brokerage or Registered Investment Advisor (RIA) arrangement model. Traditionally credit unions have implemented a third party brokerage model, however the RIA model presents several distinct advantages that align more closely with the cooperative values and member-focused ethos of credit unions. RIA vs. Brokerage

The terms brokerage and RIA are often used interchangeably, however there are key differences between the two models largely centered around standards, compensation, services provided, and member relationships. Fiduciary Duty vs. Suitability Standard: RIAs: Are held to a fiduciary standard. The fiduciary standard requires an advisor to prudently act in the best interest of members when providing financial advice. The fiduciary standard cannot be waived or disclosed away. Brokers: Are held to a suitability standard. The suitability standard requires that a broker only needs to check the suitability of a prospective product, based primarily upon financial objectives, current income level and age, in order to complete a commissionable transaction. A useful analogy popularized by financial blogger Michael Kitces is: “Suitability means selling a suit that fits you. Fiduciary duty means it actually has to look good on you, too." Compensation Models: RIAs: Typically earn income through fees, which can be structured as a percentage of assets under management, flat fees, or hourly fees. This fee-only structure is seen as aligning the advisor’s interests with those of the client. Brokers: Often receive commissions based on the products they sell or trade. This can lead to potential conflicts of interest if the broker is incentivized to sell products that generate higher commissions. Members are often unaware of many non-transparent or complicated fee products. Nature of Services: RIAs: Generally provide more comprehensive financial planning and investment management services. This includes estate planning, retirement planning, tax strategies, and more holistic wealth management. Brokers: Primary role is to facilitate the buying and selling of securities. While some brokers also offer advisory services, their core function is more transactional. Client Relationship: RIAs: Often build long-term relationships with clients, focusing on ongoing financial planning and investment management. Brokers: Client relationships are often more transaction-based, centered around specific investment purchases or sales. It is crucial to understand the operating differences between a RIA and brokerage model when selecting a wealth management program for members.  Key Updates on the Economy & Markets Financial markets underwent a sizeable shift in the fourth quarter. Treasury yields, which spiked in Q3, reversed lower as inflation eased and the Federal Reserve hinted at interest rate cuts in 2024. The decline in interest rates was a significant tailwind for stocks and bonds. The S&P 500 gained +11.6% during the quarter, and bonds produced their best quarterly return since Q2 1989. This letter recaps the fourth quarter, discusses the decline in Treasury yields and the potential for interest rate cuts, and looks ahead to 2024. Treasury Yields Reverse Lower in Fourth Quarter

Following a significant increase in Q3, Treasury yields moved sharply lower in Q4. Figure 1, which compares the change in yields during the two quarters, graphs the opposing interest rate moves. The gray bars show yields increased in Q3, with longer maturity yields rising the most. In contrast, the navy bars show yields reversed sharply in Q4, erasing nearly all their Q3 rise. The abrupt reversal can be attributed to a significant change in the market’s view heading into 2024. Investors had two key concerns, both of which contributed to the rise in Treasury yields during Q3. First, the U.S. economy continued to outperform expectations, which raised concerns that the Federal Reserve might need to keep interest rates high for an extended period to cool inflation. Second, the fiscal deficit was growing quickly as government spending increased. Investors were concerned the U.S. Treasury would need to issue a large amount of new debt to finance the growing deficit but that there wouldn’t be enough buyers for the new bonds, potentially causing yields to rise if supply outweighed demand. A notable shift occurred in November, setting off a sharp reversal in Treasury yields. Investor worries about increased Treasury bond issuance were alleviated as the U.S. Treasury revealed plans to slowly increase bond issuance. The market felt there would be enough demand to absorb the new bonds, lowering the probability that too much bond supply would cause yields to rise. In addition, data showed that inflation continued to decline even as the economy continued to exceed expectations. Investors’ fears about persistent inflation and high interest rates faded from view, and yields declined. With Inflation Falling, Market Expects Rate Cuts Data shows that inflation pressures continue to ease. Figure 2 graphs the year-over-year change in headline and core inflation. Headline inflation, which peaked at 9.1% in June 2022, dropped to 3.1% in November 2023. Likewise, core inflation, which excludes the volatile categories of food and energy, now stands at 4.0% after peaking at 6.6% in September 2022. The price declines have been widespread across categories, with price pressures easing across food, energy, airfares, and household furnishings and appliances. |

Categories |

RSS Feed

RSS Feed

© 2024 Polaris Financial, LLC.

Advisory services offered through Polaris Financial, LLC. Polaris Financial, LLC is a SEC registered investment advisor. 6 Liberty Square #2663 Boston, MA 02109. All rights reserved. Brokerage services provided to clients of Polaris Financial, LLC by Altruist Financial LLC and/or Interactive Brokers Group, registered broker-dealers and members FINRA/SIPC. Past performance is no guarantee of future results. All securities involve risk and may result in loss. Nothing in this communication should be construed as a solicitation or offer, or recommendation, or advice to buy or sell securities or services.

Investments in securities: Not FDIC Insured - Not NCUA Insured - No Bank Guarantee - May Lose Value.

Polaris Financial has a partnership with banks and credit unions to provide investment advisory services to their customers and members. The banks and credit unions are not investment clients of Polaris Financial but have a revenue sharing relationship that can create a conflict of interest.

Advisory services offered through Polaris Financial, LLC. Polaris Financial, LLC is a SEC registered investment advisor. 6 Liberty Square #2663 Boston, MA 02109. All rights reserved. Brokerage services provided to clients of Polaris Financial, LLC by Altruist Financial LLC and/or Interactive Brokers Group, registered broker-dealers and members FINRA/SIPC. Past performance is no guarantee of future results. All securities involve risk and may result in loss. Nothing in this communication should be construed as a solicitation or offer, or recommendation, or advice to buy or sell securities or services.

Investments in securities: Not FDIC Insured - Not NCUA Insured - No Bank Guarantee - May Lose Value.

Polaris Financial has a partnership with banks and credit unions to provide investment advisory services to their customers and members. The banks and credit unions are not investment clients of Polaris Financial but have a revenue sharing relationship that can create a conflict of interest.